The Definitive Guide to AI-Powered Bank Statement Data Extraction: Unlocking Unmatched Accuracy for Financial Due Diligence

In the high-stakes environment of financial services, reliance on manual data entry from financial documents is an untenable risk. This comprehensive guide is built for the financial professional—the analyst, the investor, the loan underwriter—who must move beyond fragile template-based OCR. Discover how next-generation AI-Powered Bank Statement Data Extraction is fundamentally reshaping Financial Due Diligence, driving Loan Underwriting Automation, and delivering the verified data integrity required for secure, high-volume decisions.

I. The Central Problem: Why Financial Data Extraction Is a Global Bottleneck

The sheer volume of documents that flow through a bank, a lending institution, or an investor's office is staggering. The bank statement remains the single most verified, comprehensive, and crucial source of financial truth about any individual or business. Yet, ironically, extracting usable, structured data from this critical PDF is often the slowest, most failure-prone step in the entire financial workflow.

A. The Inevitable Failure of Template-Based Systems: A Legacy Burden

For decades, the industry standard was using basic OCR (Optical Character Recognition) paired with hardcoded templates. This approach operates under a flawed premise: that document layouts are static and predictable. This has proven to be the greatest source of operational fragility and risk in document processing.

Why do these legacy systems—the very foundation of older automation—constantly fail when precision is required?

- The Format Diversity Crisis: Banks, credit unions, and various financial apps all utilize proprietary, non-standardized statement layouts. A lender servicing clients nationwide will receive statements from dozens of institutions, each with unique fonts, column structures, and date formats. Each variation requires a separate, time-consuming template to be created and maintained.

- The Change Factor: Banks routinely update their branding, rearrange tables, or adjust margins. Even a minor cosmetic change—a slightly resized transaction table or a new disclaimer at the bottom—can cause a template to miss transactions, throw off column alignment, and lead to a critical OCR template failure. The resulting downtime often forces the process back to square one.

- The Scan Quality Hurdle: Template-based systems are optimized only for pristine, digitally generated PDFs. When a customer uploads a blurry, crooked photo taken on a smartphone (a common scenario), the system loses its fixed coordinates and produces unusable, scrambled output. This means that a large percentage of incoming documents automatically default to manual data extraction.

The consequence of this failure cycle is devastating. You are paying a highly trained financial professional to stop analyzing risk and start typing numbers. This not only dramatically increases labor costs but, more critically, introduces unavoidable human error into your most sensitive datasets. For any firm aiming for scale, this manual dependency is simply not sustainable.

B. The True Cost: Risk, Not Just Time

For institutions dealing with high-stakes lending and large-scale investment, the cost of faulty data transcends wasted time; it is measured in bad loans, missed fraud, and potentially severe regulatory penalties. Data inaccuracies are not just typos; they are systemic risks that directly undermine robust Financial Due Diligence and expose the firm to substantial financial loss. This is why reliable, industry-leading financial data extraction is now a critical front-office imperative.

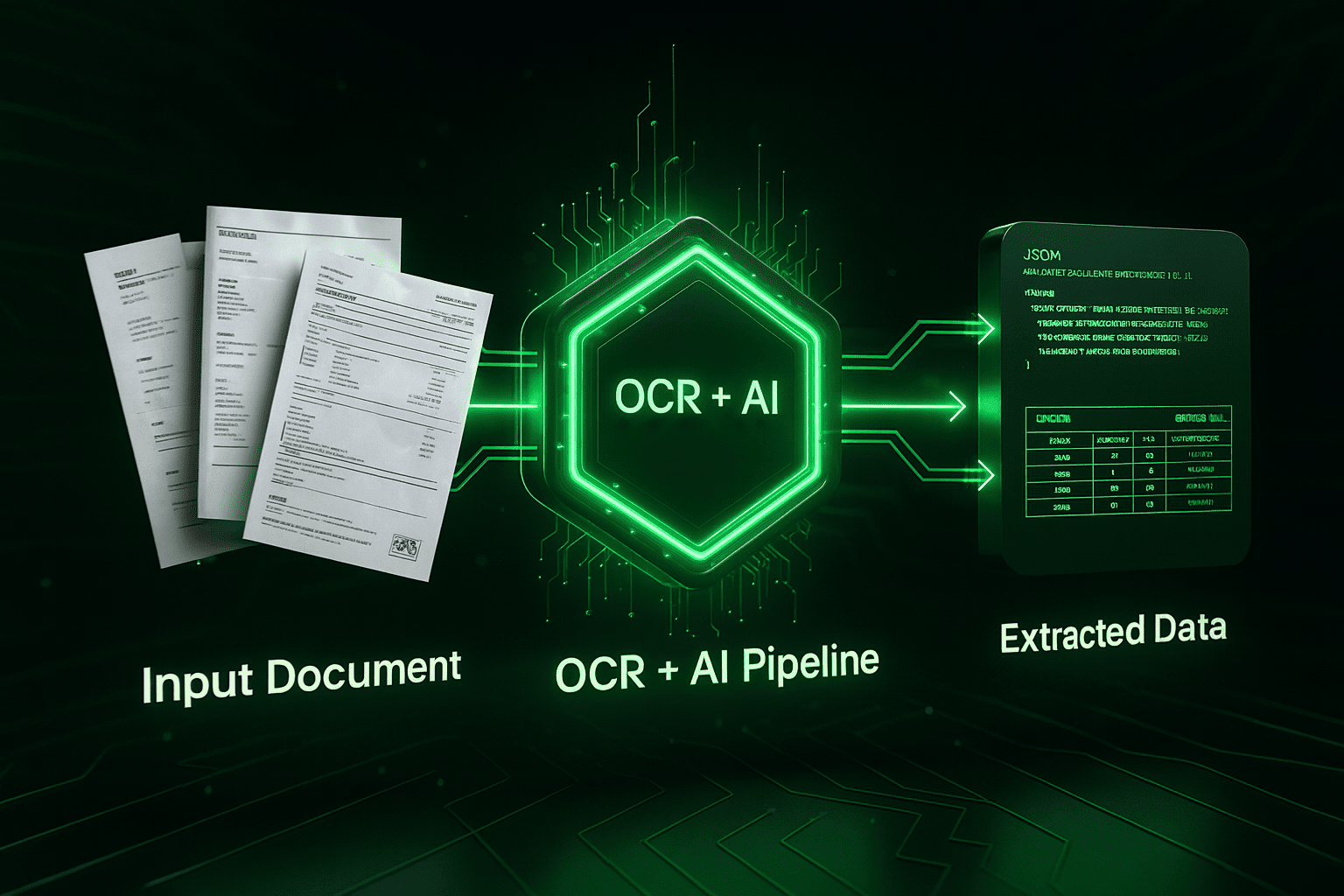

II. The Paradigm Shift: AI-Powered Intelligent Document Processing (IDP)

The future of document automation is not about building a better template; it’s about replacing the template entirely. Intelligent Document Processing (IDP) utilizes a combination of advanced Machine Learning (ML), Deep Learning, and Natural Language Processing (NLP) to replicate the comprehensive, analytical mind of a seasoned financial analyst.

A. Semantic Understanding: Reading the Document’s Mind

The core difference between old OCR and new IDP lies in the shift from identifying location (spatial recognition) to understanding meaning (semantic understanding).

Legacy OCR systems are rigid. AI-powered IDP is flexible and contextual. It learns to identify the meaning and context of data fields—such as "Transaction Date" or "Ending Balance"—regardless of their position, font, or color.

| Feature | Legacy Template-Based OCR | Modern AI-Powered IDP (Statement Extract) |

|---|---|---|

| Data Focus | Fixed X/Y Coordinates; static text strings. | Semantic keywords, tabular structures, and contextual relationships. |

| Resilience to Change | Very Low. Fails on new layouts, formatting shifts, or poor scans. | Very High. Adaptable to virtually any format, including scanned documents. |

| Verification | None. Requires separate, manual reconciliation. | Built-in reconciliation checks and fraud scoring. |

| Output | Raw, unverified text that requires manual cleanup. | Verified, normalized, and structured data in CSV or JSON. |

This template-free approach is the only way to achieve reliable and consistent data quality across the vast array of statement variations encountered in real-world finance.

B. The Three Pillars of Data Integrity and Verification

A high-performing bank statement data extraction pipeline must be a multi-stage process, ensuring data is not only extracted but also validated and certified:

- Pre-Processing and Noise Reduction: The AI first addresses the quality of the input. It automatically detects if the image is skewed or blurry, and applies sophisticated filters to deskew the image and enhance contrast. This vital preparation ensures that even low-quality, scanned bank statements are readable, setting the foundation for high data quality.

- Contextual Extraction and Normalization: The AI extracts all key fields—account information, starting and ending balances, and the complete transaction ledger. Crucially, it then normalizes the data. This involves reconciling variations in transaction descriptions (e.g., "WDL-ATM" vs. "ATM Withdrawal") into a single, standardized category. This step is essential for producing clean, unified financial data extraction ready for immediate analysis.

- Cross-Validation and Risk Scoring: This is the critical trust layer. The system performs immediate reconciliation checks: Does the extracted starting balance plus the net activity (total credits minus total debits) mathematically equal the ending balance? If the figures do not tie out—a strong indicator of error or tampering—the document is immediately flagged as suspicious. This provides an essential layer of assurance against errors and protects against systemic risk.

III. Loan Underwriting Automation: The Competitive Advantage

For lenders, AI-powered bank statement data extraction is the core engine of Loan Underwriting Automation. In today's competitive environment, the ability to shorten the time-to-decision while simultaneously mitigating risk is the ultimate form of ROI.

A. Eliminating the Manual Income and Debt Verification Bottleneck

Loan officers dedicate a substantial portion of their workload to building a comprehensive picture of an applicant's financial stability, focusing primarily on income verification and the calculation of key risk ratios.

- Manual Process: Underwriters manually struggle to distinguish between consistent salary deposits, one-time cash infusions, and recurring payments, leading to delayed or inaccurate income assessments. Furthermore, manually calculating Debt-to-Income (DTI) or Debt Service Coverage Ratios (DSCR) across dozens of transactions is incredibly time-consuming and error-prone.

- AI Process: The AI automatically categorizes transactions using ML-learned logic, efficiently isolating regular salary credits and distinguishing them from non-recurring deposits. The system instantly calculates and verifies monthly and annualized income, providing the underwriter with a clean, defensible number for their decision. This radically shrinks the underwriting cycle.

This capability transforms the underwriter's role from a tedious data typist to a strategic decision-maker, enabling true automation and scaling the lending operation.

B. Advanced Risk and Cash Flow Analysis in Seconds

The IDP system transforms the raw data within the bank statement into a real-time risk profile, essential for secure credit assessment:

| Risk Indicator | Traditional Manual Review | AI-Powered IDP Analysis |

|---|---|---|

| NSF/Overdraft Count | Manual search and count across all pages and dates (High Error Risk). | Instantaneous count, calculation of frequency ratio, and flagging of time period clustering. |

| High-Risk Transaction Types | Requires manual identification of specific merchant names and descriptions. | Automated flagging of specific, high-risk transactions (e.g., Payday Loans, excessive gambling) via ML classification. |

| Balance Trends & Volatility | Requires exporting to Excel and manually generating a graph. | System-generated summary of balance volatility, identification of sudden drops, and cash flow forecasting indicators. |

This detailed, data-driven approach allows lenders to make a credit decision in minutes, not days, drastically improving the borrower experience and reducing operational costs while adhering to strict lending guidelines.

IV. Securing Capital: AI for Financial Due Diligence and Fraud Prevention

For investors, auditors, and private equity firms, Financial Due Diligence (FDD) is where the highest risk resides. The slightest error in a target company's financials can compromise the entire investment thesis. Here, data extraction must prioritize verification over simple extraction.

A. The Critical Battle Against Synthetic Fraud and Tampering

The market for forged or fake bank statements is increasingly sophisticated. Simple visual checks are now insufficient against advanced digital manipulation. The best defense is an AI-powered fraud detection system that performs non-human checks at the pixel and metadata level:

- Structural Tampering Detection: The AI analyzes the PDF's internal metadata and code structure. It checks if the document has been digitally altered, or if the internal font properties and table structures are consistent with the claimed bank. It flags inconsistencies that suggest the document was edited and saved outside of the original banking system.

- Micro-Pattern Anomaly: The system is trained on the statistical noise and irregularities inherent in real-world banking. It flags transactional patterns that are "too perfect," such as perfectly rounded deposits every single week without fail, or transactions that lack the necessary bank-specific codes, which are strong indicators of fabrication or synthetic fraud.

By leveraging this profound layer of financial fraud detection, investors gain a crucial, early warning system to safeguard their capital and ensure their investor due diligence process is built on highly verifiable facts.

B. Achieving Comprehensive Coverage Across the Financial Review Spectrum

True IDP must extend beyond bank statements to provide a unified financial data extraction software solution for all records required in FDD. This eliminates the need for multiple single-purpose tools and ensures a consistent standard of data quality across all documentation:

- Tax Form Data Extraction: Process complex documents like W-2s, 1099s, and corporate tax returns for formal income proof and liability assessment. The AI understands the regulatory-specific fields and rules, which is impossible with generic OCR.

- Invoice Processing: Automate Accounts Payable (AP) and cost analysis workflows by reliably pulling line-item details, vendors, dates, and totals from diverse and often highly varied invoice formats.

- Proof of Funds Verification: Quickly process brokerage statements, saving accounts, and other asset documents to verify the total capital available to the individual or business being reviewed.

The ability to process all unstructured data from these diverse sources with a single, template-free engine ensures a faster, more comprehensive, and trustworthy financial audit.

- Automated Bookkeeping: Stop manually keying in transactions. If you're still relying on rudimentary tools, learn why your team should stop wasting time on manual PDF conversion and adopt an AI solution instead.

V. Strategic Implementation: From Legacy Risk to API-Driven Trust

Moving from a manual, legacy process to AI-driven automation requires a clear, secure, and scalable implementation path.

A. The User Journey: Simple, Fast, and Integrated

The process must be simple enough for immediate adoption across operational teams, requiring minimal training:

- Upload: Securely upload single or bulk PDFs (or scanned images) of the financial documents through a web interface or dedicated portal.

- Processing: The AI instantly analyzes, corrects, extracts, normalizes, and verifies the data. The entire pipeline, including reconciliation checks, runs in seconds.

- Review (Exception Handling): The system flags only high-risk documents or low-confidence extractions, directing the analyst’s attention only to the necessary exceptions. This practice significantly reduces the total review time.

- Export & Integration: The clean, structured, and verified data is exported in the user's preferred format: CSV, Excel, or directly into target systems via a robust, secure API.

B. The Power of the Financial Data Extraction API

For high-volume organizations (banks, large accounting firms, FinTech platforms), the API integration is the operational core. It allows for straight-through processing (STP) where documents are uploaded via a secure endpoint, processed in real-time, and the verified data is instantly piped into a Loan Origination System (LOS), a CRM, or a proprietary analytics engine.

This eliminates the need for manual file downloads and uploads entirely, which is essential for maximizing throughput and achieving true, measurable operational scalability. The API serves as a developer-friendly bridge, enabling organizations to leverage external financial data with the same speed and integrity as internal database information.

Try StatementExtract for Free Today

C. Security, Compliance, and Data Trust: The Non-Negotiable Factors

In the financial industry, security is the foundation of trust. Any provider of financial data extraction software must adhere to the highest global standards:

- Data Encryption: All documents and extracted data must be protected with end-to-end encryption—in transit (via TLS/SSL) and at rest (using industry-standard encryption protocols).

- Compliance Frameworks: Strict adherence to regulatory requirements like GDPR, CCPA, and SOC 2 principles is crucial. This proves a commitment to data integrity and secure handling practices.

- Data Control and Ownership: Users must maintain absolute control over their data. Clear policies on data retention, deletion, and the assurance that client data is never used for unauthorized internal model training are essential components of the trust relationship.

Building a solution with these principles at the forefront is how a provider establishes the necessary Expertise, Authoritativeness, and Trustworthiness (E-E-A-T) required for top-tier financial service delivery.

VI. Final Analysis: Calculating Your Definitive ROI from IDP

The financial case for adopting advanced AI-powered bank statement data extraction is now driven by three measurable pillars of return:

- Time Savings and Efficiency: Reduce the overall manual entry and review time from an average of 30 minutes per document to 1 minute or less, effectively reallocating highly compensated financial analysts to focus on decision-making, not data entry.

- Risk Reduction and Capital Protection: Minimize financial losses from undetected fraud, and drastically reduce regulatory exposure due to human data errors. This preventative ROI is often the single most valuable contribution, securing millions in capital.

- Scalability and Competitive Advantage: Enable high-volume processing and massive client onboarding without needing to proportionally increase internal headcount or bear the constant maintenance cost of template systems. The speed of decision-making becomes the competitive edge.

The reality is that your competitive future hinges on your speed and accuracy. The shift from fragile, template-based legacy systems to flexible, AI-driven solutions is no longer optional—it is required to manage operational risk and seize market opportunities.

Ready to Transform Your Financial Decisions?

Stop building fragile templates and start leveraging verified, AI-powered data extraction. Unlock the speed, accuracy, and competitive edge required for modern Financial Due Diligence and Loan Underwriting Automation.

Frequently Asked Questions (FAQ)

This section targets common informational and commercial investigation keywords to capture users late in their research journey.

Q1: What is the primary difference between traditional OCR and AI-Powered IDP for financial documents?

A: The primary difference is contextual understanding. Traditional OCR only converts text on a page to digital characters, relying on rigid, pre-defined templates to guess where data is located. AI-Powered IDP (Intelligent Document Processing) uses Machine Learning to understand the semantic meaning of the text. It recognizes that "07/15/2025" next to the label "Ending Balance" is a date and knows what an ending balance is, regardless of where it is positioned on the statement. This template-free approach is why IDP achieves superior, industry-leading accuracy on variable formats.

Q2: How does your system ensure data quality and integrity without claiming 100% accuracy?

A: We focus on Data Verification and Risk Scoring rather than unrealistic claims. Our system ensures integrity by running comprehensive, non-negotiable reconciliation checks (e.g., verifying that the extracted starting balance plus net transactions equals the ending balance). Any document that fails this check or shows signs of tampering is automatically flagged, allowing your analysts to focus only on high-risk exceptions.

Q3: Can your system handle bank statements that have been scanned or are of low quality?

A: Yes. Unlike template-based solutions that fail on distorted images, AI-powered IDP incorporates a vital pre-processing stage. This stage automatically corrects skewed images, reduces background noise, and enhances text contrast. This ensures that even low-quality, scanned bank statements are readable and processable, making the data extraction reliable for all your input sources.

Q4: How does AI help in detecting fake or fraudulent bank statements?

A: AI provides a powerful layer of financial fraud detection. Beyond simple data extraction, the system is trained to identify anomalies that signal fraud. This includes detecting structural manipulation in the PDF's internal code, flagging transactions that are statistically too perfect, and verifying that the transactional data reconciles with the final balances, offering essential protection for investor due diligence.

Q5: What data formats do you export for easy integration with existing financial systems?

A: For immediate use and easy integration, the verified, structured data can be exported in the most common analytical formats: CSV (ideal for Excel), JSON (for developers and APIs), or directly into your internal systems via a simple, robust API integration. This allows for seamless accounting software integration into any existing LOS, CRM, or data warehouse.